Here's a simple tip, which may help some clergy looking to complete their tax returns.

Disclaimer: I am not an accountant, so this is not professional advice, merely a tip from a fellow traveller. Needless to say, you are responsible for the figures you put on your own annual returns.

A perennial frustration

There's a cycle that repeats each year.

TL;DR — We have to wait for a P11D, so can't complete a tax return, so can't renew tax credits, so have 3 months of the year when our tax credit payments are down.

Clergy have to complete a self-assessment tax return each year.

Amongst other sections, they need to complete the "Minister of Religion" page.

To do this, they need two source documents: The P60 (end of tax year payment summary) and P11D (showing taxable benefits from an employer). In the 2016-17 form, it's box M of the P11D that needs to go into Box 13 of the Minister of Religion page.

Some clergy may have very complex forms P11D. Most of us only have one figure on the P11D, showing the total figure from the relevant year that has been paid tax-free under the HLC (Heating, Lighting and Cleaning) scheme.

The Church Commissioners send out the P60 forms promptly, soon after 5th April. However the statutory deadline for employers to send out P11D is not until 5th July. The Church Commissioners usually do not send these out until the last week in June, just before that deadline.

This is very frustrating. For clergy on the simplest finances, the Commissioners have had the necessary figures since 31st March. Yet, without a P11D, we cannot complete our tax returns.

What's more, the income declaration for a Tax Credit renewal needs the bottom line figure (currently box 38) from the Minister of Religion page. So, no P11D, no tax return; no tax return, no Child or Working Tax Credit renewal.

The deadline for renewing Tax Credits is 31st July. That leaves just under 4 weeks from the latest date that the P11D could be sent out.

Meanwhile, from 5th April onwards, HMRC will temporarily reduce tax credit payments for those who have not yet completed a return. This is for the benefit of those who never submit an annual return; HMRC are keeping down the amount they'd have to repay. But, for those who are waiting for their P11D, it means lower payments until the annual renewal can be put through. Once you do renew, HMRC will pay the full amount, so you don't end up short long-term, but for some clergy these temporarily lower payments could cause real hardship.

A Plea to the Church Commissioners

I know that, by law, you don't have to send out the P11D until 5th July.

But is there not some way where these can be sent out sooner, at least for the clergy whose finances don't have extra complexities?

Please?

How to Get Things Moving

In fact, if you only need your P11D for that one figure in Box M, you don't need to wait. Here's how you can get things moving.

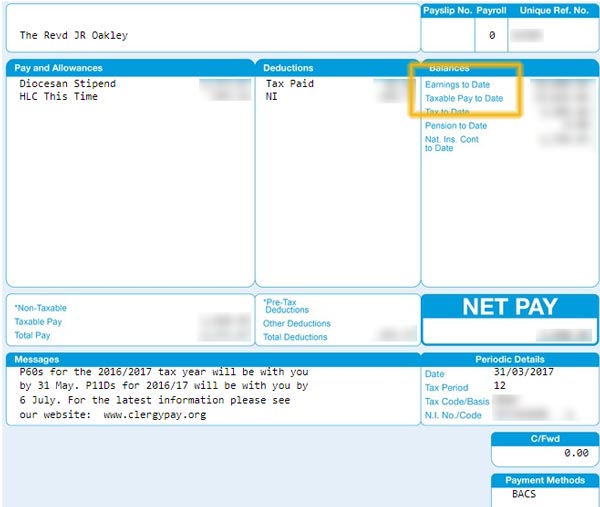

Take a look at your payslip from March 31st. It comes in three columns. The left hand column shows the money you've been paid this time. The middle column shows the deductions (tax and NI). The right hand column shows you the running total of figures this tax year.

You want the top two figures on the right hand side. As this is your last payslip of the tax year, the figures here are full-year figures, not just "year to date".

- "Earnings to Date" shows the total you've been paid for the year (before tax). It includes both the stipend on which you've been taxed under PAYE, and also the HLC costs which you've been paid without tax deducted.

- "Taxable Pay to Date" shows just the first of those - the stipend on which you've been taxed under PAYE.

If you subtract the two, and round down to the nearest pound, that will be the figure that eventually ends up in box M of your P11D.

Remember: This is Provisional

Remember my disclaimer above: I'm not an accountant.

Here's my suggestion as to what you can do with these figures.

You can use them to sketch out what your Minister of Religion self-assessment page is likely to look like. That will allow you to come up with a provisional bottom-line income figure in Box 38. Those figures are provisional, because you need the actual P11D to be certain you're using the correct figures, and that there are no other unexpected entries on this year's form.

I'd suggest you don't complete your self-assessment tax return until the actual P11D comes out. The earliest deadline from HMRC is 5th October, so you have plenty of time.

However, I'd suggest you do use this draft figure to put together the figures for your Tax Credits renewal and get that processed. There is a box you can tick that says you're sending them draft figures. Definitely tick that. And (I can't remember) if there's a free text box to say what's provisional, explain you're waiting on your P11D. That means you can get your Tax Credits renewal done promptly, and your payments won't drop while you wait.

When the P11D comes, you can then process the tax return, and check that your figures for Tax Credits were correct.

A Note for Non-Clergy

I highly doubt you've read this far if you're not a Church of England cleric. But in case you have, please don't get the wrong idea here. Some people hear about the "HLC" scheme I'm referring to, and think that vicars can pay their gas and electricity bills before income tax.

Sadly, not. I won't explain how it all works, because it's way too complex, and you're probably not that interested. But suffice to say: The HLC isn't taxed on the payslip, but you do end up paying tax on most of it once your tax calculation's gone through. HMRC know this, so they factor typical figures into your tax code. This means that, when income tax is calculated for your actual taxable pay, your personal allowance has already been reduced, and the PAYE calculations mean you effectively do pay tax on everything including the HLC. All the year-end tax return does is check if there's a balancing payment due in either direction.

How it works

Hi Michael

Thanks for reading, and for commenting.

Standard disclaimer: I'm not an accountant, so nothing I'm about to write constitutes advice. Anyone declaring their Minister of Religion income to HMRC is responsible for their own figures.

It is more complex yes, but it's still a great scheme.

What happens is that the HLC component of your gross stipend is not included when tax and NI are calculated by the Commissioners on your monthly payslip. So, effectively, you get the HLC component free of tax and NI.

However, when you complete your tax return, you find you have to declare it back as a "benefit in kind" that you've received. So your HLC amount is a taxable benefit, so you end up paying tax on it after all.

Except you don't quite. Follow the MoR page notes to see how this works exactly, but in outline:

- In box 25, you get to deduct 25% of your HLC amount as other expense you have had to pay as a minister of religion. (I think the explanation for this is that, roughly, a quarter of the HLC is for the "work" part of the parsonage house you occupy).

- You do have to pay the HLC figure as a benefit in kind when it comes to income tax, but the NI never gets clawed back. So even if you don't save the 20% on the HLC, you still get to keep the 11% saving. (It's funny: From time to time, the government has reduced income tax and increased NI, which has led to the accusation that NI is a stealth tax, and they can claim taxes are falling whilst in fact people pay the same amount. Clergy are one group who actually benefit from this).

- There is the "Benefit in Service Cap". Again - the calculation is complex, so follow it through. Roughly, the most you'll ever have to pay tax on (as a taxable benefit in service) is 10% of your otherwise gross income. We used to live in a draughty old vicarage that cost a fortune to heat. We easily exceeded that benefit cap every year, so we got to keep 100% of the HLC tax free once the HLC crossed the threshold of 10% of gross earnings.

So it's not as simple, nor leaves you as well off, as "all the HLC is free of tax". But it still gives a significant benefit that relates directly to the fact that some of your heating and lighting is because the vicarage is partly a public building, and also relates to ability to pay (via the cap).

Of course, in practice, if HMRC get your tax code right, you won't actually be paying it back as tax on a benefit in service. Instead, they'll adjust your tax code so that you pay slightly more tax throughout the year.

HTH

Thanks for this. I got my first P11D today from the Church Commissioners. The HLC scheme was sold to me as precisely being able to pay for Heating, Lighting and Cleaning in a tax-deductable way. I'm now looking at my estimated tax calculation and wondering what the actual benefit of the schemeis for clergy! Can you explain, please?